Stability 101

Stability 101 — Emergency Fund

If you don’t have an emergency fund yet, start here.

Stability comes from access to cash and clarity during disruption. This supports organizing emergency plans and financial documents so unexpected events don’t turn into long-term damage.

Establishing an Emergency Fund

An emergency fund is a liquidity reserve designed to absorb unexpected financial disruption.

It exists to protect:

• Income interruption

• Medical expenses

• Essential repairs

• Unexpected obligations

• Economic downturn exposure

An emergency fund is not an investment account.

It is not discretionary capital.

It is not opportunity funding.

It is structural protection.

Purpose of an Emergency Fund

Emergency reserves reduce:

• Debt reliance

• Forced asset liquidation

• Reactive financial decisions

• Cash flow instability

When reserves are established, financial decisions remain controlled during disruption.

Liquidity prevents fragility.

How to Structure an Emergency Fund

A standard framework includes:

• Starter reserve: $500–$1,000

• Intermediate reserve: 1–3 months of essential expenses

• Full reserve: 3–6 months (or more depending on income volatility)

Funds should be:

• Easily accessible

• Kept separate from daily spending

• Preserved from discretionary use

Opportunity investing should come from surplus capital — not emergency reserves.

Stability Before Expansion

Emergency funds are foundational.

Before:

• Investing aggressively

• Increasing lifestyle spending

• Pursuing speculative opportunities

Ensure liquidity is secured.

Growth without protection increases exposure.

We removed:

• Vacation language

• Reward framing

• “Possible gains”

• Emotional reassurance

• Motivational tone

Because emergency funds are defensive strategy — not lifestyle enhancement.

Available from Amazon/Kindle or directly from Truality.Finance by Mr.Why

Stability 101 — Preparing for Disruption

Why stability comes before growth — and why emergency funds are misunderstood

An ethical, simple framework

Most financial advice treats stability as an afterthought.

This guide treats it as the foundation.

Stability 101 is not about fear-based prepping or extreme conservatism. It’s about understanding why disruption is normal, why growth without stability is fragile, and why emergency funds are often misunderstood or misused.

This guide treats stability as a structural requirement, not a personality trait.

What Makes This Different

Unlike most financial content about safety nets, Stability 101:

Does not frame emergencies as rare events

Does not promote fear or worst-case thinking

Does not treat emergency funds as idle or wasted money

Does not push growth before readiness

Instead, it focuses on:

Stability before expansion

Preparation before optimization

Capacity before risk

Reality before reassurance

The goal is resilience, not acceleration.

What This Guide Helps You Do

Understand why disruption is inevitable

Reframe emergency funds as structural tools

Identify where instability actually comes from

Reduce financial fragility without panic

Build a buffer that supports calm decision-making

No fear tactics.

No overfunding myths.

No pressure to “optimize.”

Just a clear framework for staying upright when life shifts.

Who This Is For

This guide is for people who:

Feel pressured to grow before they’re ready

Have been told emergency funds are “dead money”

Want resilience without anxiety

Value ethics, realism, and long-term stability

If financial growth has felt shaky or stressful, this guide was written to explain why stability must come first.

Stability Paths: Emergency Fund Protocol

1) Define a Liquidity Target

Establish a structured reserve goal:

• Starter reserve: $500–$1,000

• Intermediate reserve: 1 month of essential expenses

• Full reserve: 3–6 months (or more depending on income volatility)

Targets should reflect fixed obligations — not comfort level.

Liquidity planning is based on risk exposure, not preference.

2) Separate Emergency Capital

Open a dedicated savings or money market account exclusively for emergency reserves.

Separation reduces behavioral leakage and prevents discretionary spending interference.

Emergency capital must remain:

• Accessible

• Liquid

• Protected from routine transfers

Reserve accounts are protective infrastructure — not flexible spending pools.

3) Redirect Cash Flow Inefficiencies

Audit income and expenses to identify structural leakage.

Common areas include:

• Underused subscriptions

• Recurring auto-renewals

• Variable discretionary spending

Reallocate recovered capital directly to reserves.

Recent survey data indicates a significant portion of households lack adequate emergency coverage. Liquidity weakness increases vulnerability during disruption.

Expense discipline strengthens reserve growth.

4) Automate Contributions

Establish automatic transfers into emergency reserves.

Automation reduces behavioral friction and improves consistency.

Liquidity grows through structured repetition — not motivation.

5) Scale Contributions Gradually

Begin with manageable recurring allocations.

Increase contributions as:

• Income stabilizes

• Debt decreases

• Expenses are optimized

Progress should be steady and sustainable.

Overextension creates new instability.

Core Principle

Emergency reserves are defensive capital.

They exist to prevent:

• Debt reliance

• Forced asset liquidation

• Reactive financial decisions

• Cash flow collapse

Growth strategies follow liquidity protection — not the reverse.

We removed:

• “Peace of mind”

• Comfort-based goal framing

• Emotional encouragement

• Personal sacrifice language

• Motivational tone

We kept:

• Structure

• Discipline

• Clarity

• Risk awareness

Emergency fund strategies:

High-Yield Savings Account: Keep cash safe but earning higher interest.

Cash + Liquidity Mix: Store most in savings, some in money market or CDs.

3–6 Months Rule: Cover essential expenses, more if self-employed.

Automate Savings: Set up direct transfers each payday.

Separate Account: Keep it apart from daily spending to avoid temptation.

👉 Goal: fast access + steady growth without risk.

$11.25)- “Your Money or Your Life by Vicki Robin – Transform how you manage money and prioritize financial security.”

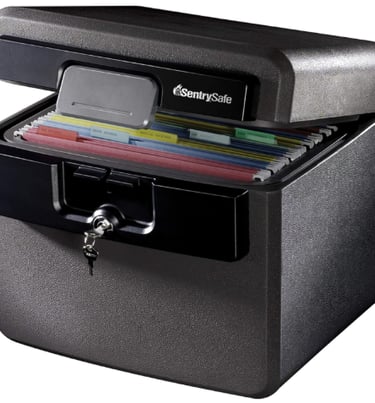

$56.14)- SentrySafe Fireproof & Waterproof Safe Box – Keep cash, documents, and valuables secure from disasters.

$11.99)-Financial Freedom Made Easy: Step-by-Step Guide to Eliminate Debt, Create a Financial Plan and Provide Security for you and your Family

$22.99)- Clever Fox Savings & Emergency Planner – Track your savings milestones and stay motivated to reach your financial goals.

$13.99)- “Set for Life by Scott Trench – Learn how to escape the paycheck-to-paycheck cycle and build a secure emergency fund.”

$8.99)- Emergency Cash Envelopes Set – Organize and protect backup funds for home or travel use.

Affiliate Disclaimer: "As an Amazon Associate, Mr. Why’s Safety Net Saturday earns from qualifying purchases. Your support helps keep our financial lessons free—at no extra cost to you.”

“Mr. Why’s Safety Net Saturday: Smart Amazon Finds to Secure Your Financial Peace”

$16.29)- First Aid Only 260-Piece Kit — a reliable, all-purpose first aid box with plenty of supplies for home, work, or your car. It’s organized, easy to use, and gives you peace of mind knowing you’ve got the essentials covered if something unexpected comes up.

$36.54)- Ready America 72-Hour Emergency Kit — a solid 2-person go-bag with the basics you’d want for a few days. It’s easy to grab, good for the car, camping, or unexpected situations, and comes with first aid supplies and blankets to keep you ready wherever you go.

$29.99)- Car Roadside Emergency Kit — Complete auto safety pack with jumper cables, safety hammer, reflective triangle, tire-pressure gauge, tow rope, and more essential tools for roadside emergencies.

$247.00)- 4Patriots 4-Week Survival Food Kit — A dependable emergency supply with 192 servings and a 25-year shelf life. A solid choice for peace of mind and long-term readiness.

$15.99)- A fun little Emergency Fund box that keeps saving lighthearted. Add your own ideas, goals, or surprises — and ‘break in case of emergency’ when life hits you with something unexpected. A simple reminder to build your safety net. Full details on the blog — link in bio.”

$180.00)- A complete 3-day Emergency Bag designed for earthquakes, hurricanes, wildfires, floods, and anything life throws your way. A simple, smart way to protect yourself and the people you care about. For the full breakdown, check my blog site — link in bio.

$32.00)- Medical Guardian MGMini

a simple, water-resistant emergency alert device for seniors. Features a quick call button, 24/7 monitoring, step tracking, and GPS support. Requires a monthly subscription. Color: Pearl.

$34.95)- Smarter LifeStyle Elegant Medical ID Bracelet

durable surgical-steel design with “No Needle, No BP This Arm” engraving. Comfortable, stylish, and ideal for quick medical identification.

$99.00)- Ridge Wallet for Men

a slim, minimalist card holder with RFID protection and a front-pocket design, complete with a carbon-fiber cash strap.

$9.99)- Sukuos Large Weekly Pill Organizer

a simple, easy-open AM/PM pill case with double protection. Perfect for keeping your vitamins, meds, and supplements organized all week without hassle.

$9.99)- Amazon Basics Emergency Seat Belt Cutter and Window Hammer Tool

A simple but essential car safety tool designed to help in emergencies. This 2-pack includes a seat belt cutter and window hammer to help you escape quickly if you’re ever trapped in a vehicle.

BLAVOR Solar Power Bank 10,000mAh

A reliable portable power bank designed for everyday use and emergencies alike. With 10,000mAh capacity, fast 20W charging, wireless charging support, and solar panel backup

“Find out how much cash you should set aside for unexpected expenses. Enter income, bills, and risk level to get a clear target.”

Crisis

Mr. Why provides structured financial strategies focused on stability and disciplined execution. Supporting resources are included where appropriate to assist with implementation. Long-term financial control is built through consistent application of sound principles.

Emergency Fund: Financial Security Through Liquidity

An emergency fund is a dedicated liquidity reserve designed to absorb unexpected financial disruption.

It protects against:

• Medical expenses

• Vehicle repairs

• Income interruption

• Urgent household obligations

Without liquidity reserves, unexpected expenses often lead to high-interest debt or forced asset liquidation.

Emergency funds reduce dependency on credit and preserve financial stability during disruption.

Determine the Appropriate Amount

A common benchmark is three to six months of essential living expenses.

The appropriate reserve size depends on:

• Income stability

• Employment risk

• Fixed monthly obligations

• Household dependency structure

This buffer provides operational flexibility during temporary financial disruption.

Structured Implementation

Building a full reserve may take time.

Begin with:

• A starter target ($500–$1,000)

• Gradual scaling toward one month of expenses

• Expansion to three to six months as income stabilizes

Progress should be measured and sustainable.

Liquidity strength increases resilience.

"The Truality Cause', the brand that is dedicated to integrity, transparency, and delivering accurate, trustworthy content to empower our users."

© 2025. All rights reserved.

"Dedicated to Helping You Build Your Financial Future". Please, feel free to subscribe to our newsletters, updates, and special offers!

2025> please be informed site was AI assisted ⚠️ Content Integrity Protected

🔒 User-Secured Validation

🔒 AI-Assisted Content Notice > Portions of this website's content have been generated or enhanced using artificial intelligence tools. While efforts are made to ensure accuracy and reliability, AI-generated content may contain errors or inaccuracies. Users are encouraged to verify information and consult professionals for advice. [TRUALITY] is committed to transparency and content integrity. Please report to us any concerns.

© 2026 MrWhy Consulting - SaaS

"An Expert In Psychology, Law & Finance!"

“My work is descriptive and analytical — focused on understanding patterns, not prescribing universal solutions.”

The Anti-Shark

“I’m here to Make you money, not take it.”

“I’m here to help, not exploit.”

"Remember to Stay Steady, Stay Real, and Stay You!"